Key facts.

- IMF Note 2026/004 on agentic payments identified "success divergence" as a systemic risk: AI agents treating payment authorization as terminal success when authorization and settlement are distinct steps across most payment rails (IMF Note 2026/004, imf.org).

- ISO 20022 payment messaging standards distinguish explicitly between payment order acceptance, clearing confirmation, and settlement finality - three distinct events that most agent integrations treat as one.

- Card network payment flows include authorization, clearing, and settlement as distinct phases separated by up to 72 hours, with chargeback windows that can extend 120 days after apparent settlement - all invisible to agents that stop at authorization confirmation.

- ACH and wire transfer rails have settlement windows of 1-3 business days, creating a gap of 24-72 hours between agent success confirmation and actual fund availability that most agent architectures cannot track.

- Post-incident analysis of agentic payment failures typically finds that the agent correctly called the payment API and correctly received the authorization response - the failure was in the definition of "success," not the API call mechanics.

Why authorization is not success in payment workflows

Authorization tells you the bank validated the card, confirmed the account has funds or credit available, and reserved the amount. It does not tell you the payment cleared. It does not tell you the funds settled. It does not tell you the merchant received the money. Those are separate events in the payment lifecycle, and they can fail independently.

A payment can authorize and then fail to clear because the card is cancelled before the next business day's batch. It can authorize and clear and then receive a chargeback filed by the cardholder within 120 days. It can authorize on a card that passes through multiple currency conversions with exchange rate settlement that differs from what the authorization locked in. Each of these is a legitimate outcome in production. Each looks like success to an agent that stops at authorization.

What production-ready payment agent architecture requires

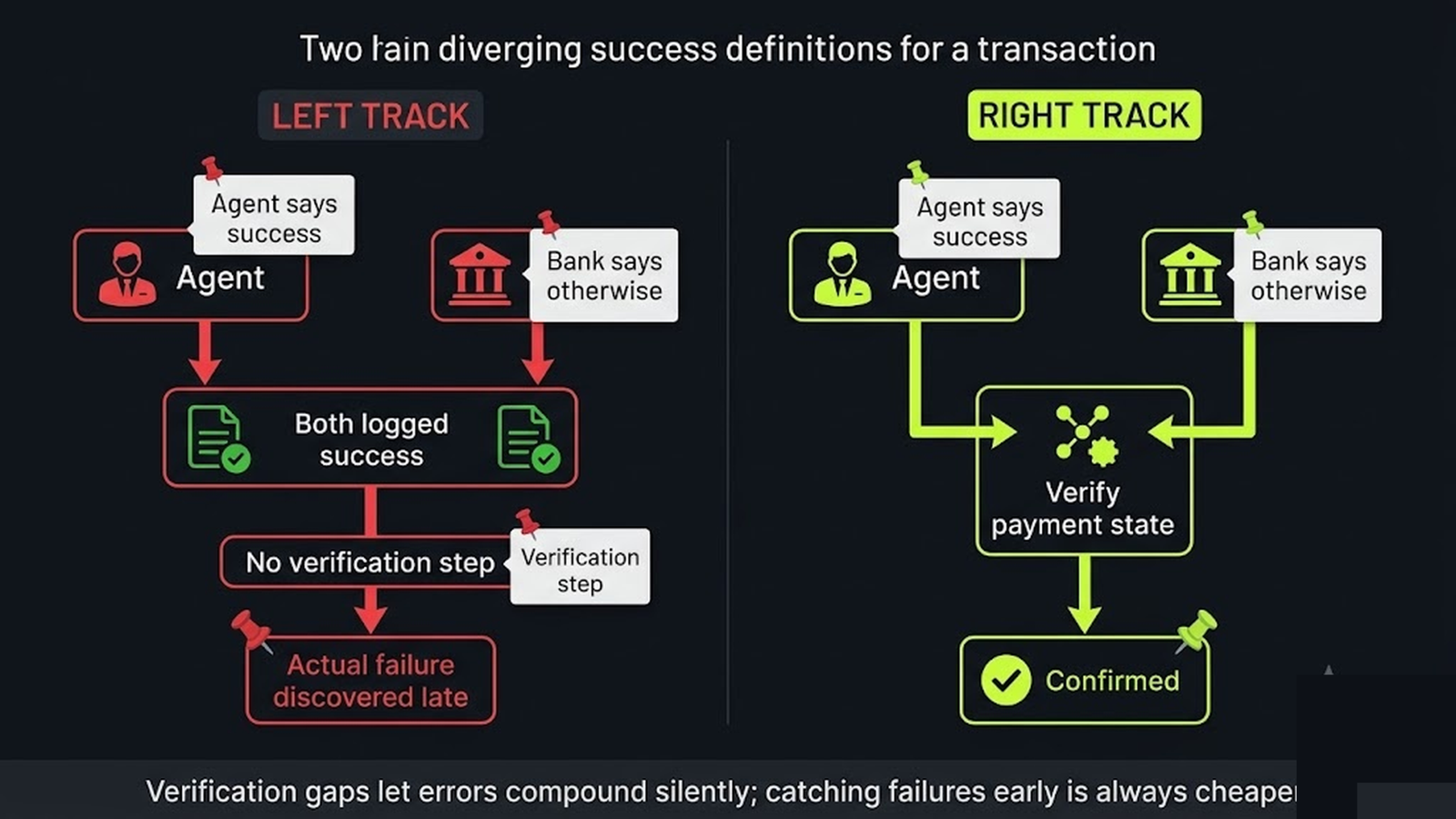

A payment agent architecture that is actually fit for production finance workflows needs to distinguish three states explicitly: authorized (reserved, not yet cleared), cleared (batch processed, not yet settled in merchant account), and settled (funds received, reconciliation window open). The agent's "success" state is settled, with reconciliation confirmation. Authorization is a checkpoint on the way to success, not success itself. This requires either a callback mechanism from the payment processor when settlement completes, or a polling job that checks settlement status independently of the agent's session, because the settlement timeline typically outlasts the agent's context window.

Payment lifecycle phases and agent visibility

| Phase | Timing | Agent typically sees | What it actually means |

|---|---|---|---|

| Authorization | T+0 to T+2 seconds | "Success" response (incorrect) | Funds reserved, not received |

| Clearing | T+hours (batch) | Nothing (session ended) | Transaction submitted to bank |

| Settlement | T+1 to T+3 days | Nothing (session ended) | Funds transferred |

| Reconciliation | T+1 to T+120 days | Nothing (session ended) | Chargebacks and disputes resolved |

IMF Note 2026/004 named success divergence: the agent closes on authorization while settlement lags, and a better model calls that state terminal. (IMF Note)

VibeModel's Pattern Intelligence Layer identifies which payment workflow patterns in your specific deployment have historically shown success divergence. By correlating authorization confirmations with settlement records from your payment processor's reconciliation data, it surfaces the authorization-to-settlement gap rate for each payment type in your integration. That data converts "we think our payment agent works" into "we know our payment agent's settlement confirmation rate is X%, and here are the flow types that diverge." That is the conversation every CFO should be having about their agentic payment systems before they scale.

Frequently asked questions

How should an agent handle the settlement waiting period without holding the session open?

Decouple the settlement confirmation from the agent session. The agent initiates the payment and records a "pending settlement" state. A background job polls the payment processor's settlement API and updates the state to "settled" when confirmation arrives. The agent or a notification system alerts the relevant stakeholder when settlement completes, not when authorization completes.

What is the minimum logging required for agentic payment regulatory compliance?

At minimum: the authorization response with full transaction ID, the clearing confirmation with batch ID, the settlement confirmation with value date, and any chargeback or dispute notifications. All should carry the same transaction ID to enable end-to-end tracing. For regulated jurisdictions (EU, US federal), these logs require retention periods of 5-7 years depending on transaction type.

Do these same phases apply to B2B wire transfers?

Yes, though the terminology differs. Wire transfers distinguish between wire order initiation, confirmation of receipt by correspondent bank, and final credit to beneficiary account. Each is a separate event that can fail independently. SWIFT gpi tracking provides near-real-time visibility into wire settlement status and is the recommended integration for B2B wire agents.