Key facts.

- GhostCite (arXiv:2602.06718) documented LLM failure to distinguish confirmed-negative from ambiguous/pending outcomes, a verification gap directly applicable to payment decline code interpretation where soft and hard declines require different responses (GhostCite, arXiv:2602.06718).

- Visa and Mastercard decline code taxonomies distinguish soft declines (01, 05, 51, 61, 65: conditions that may change with retry or customer action) from hard declines (04, 14, 41, 43: conditions requiring permanent cessation of retry). Most agent implementations treat all non-zero response codes as permanent failures.

- Stripe's public statistics indicate soft declines account for approximately 15-20% of declined transactions in card payment processing, making it the largest single category of payment failure that requires a different agent response than a hard decline.

- Optimal soft decline handling requires: (1) parsing the specific decline code, not just the binary success/fail signal, (2) mapping the code to the appropriate retry strategy (immediate retry with different network, retry after interval, request card update from customer), (3) attempting the appropriate retry, (4) verifying the retry outcome before reporting to the customer.

- SCA (Strong Customer Authentication) declines in European card transactions require a specific 3DS challenge flow before retry - a multi-step verification process that most agent payment integrations do not implement for declined transactions.

Why soft declines expose the verification gap most clearly

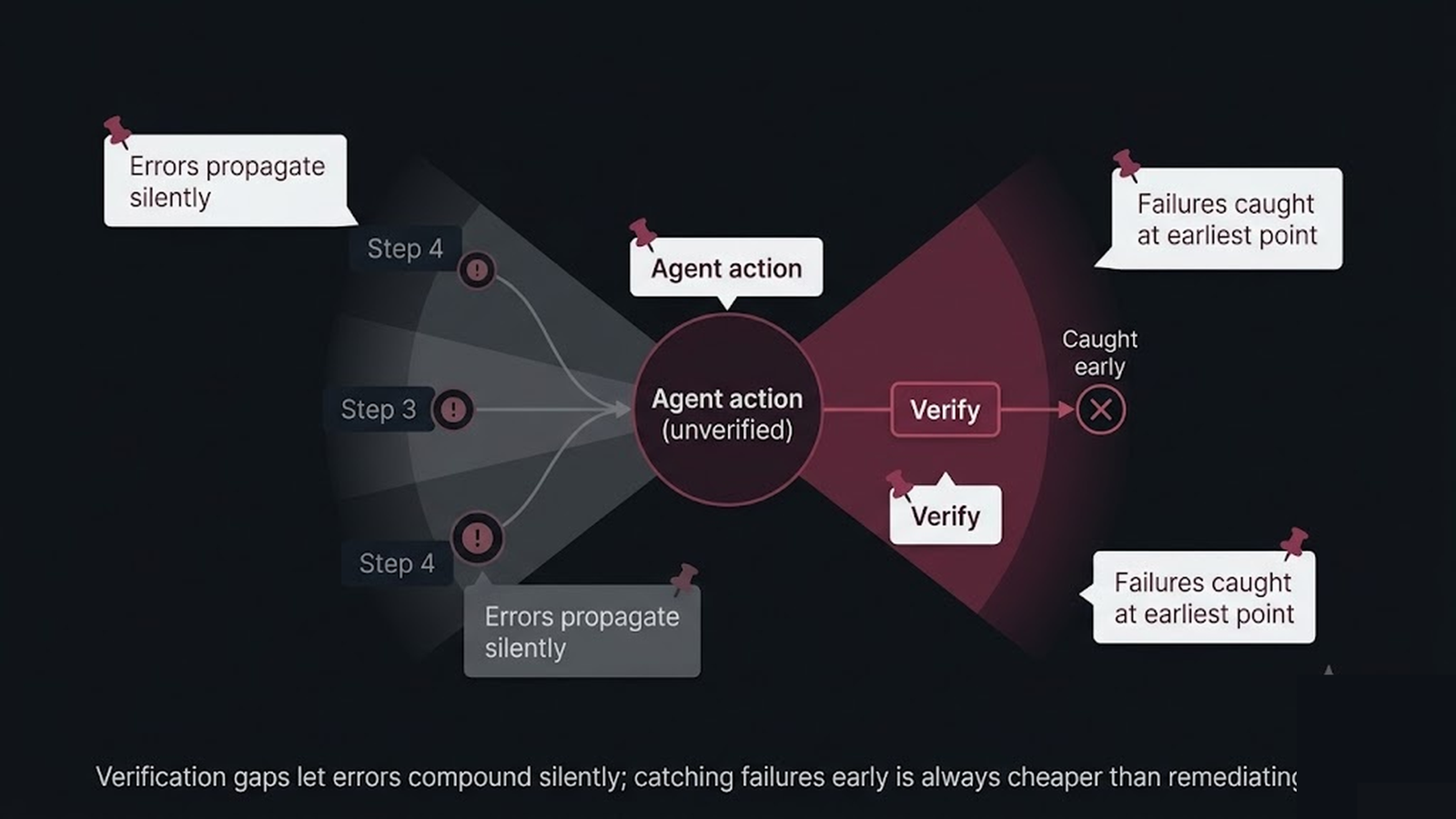

A hard decline is unambiguous: the payment cannot proceed with this payment method. The agent's correct response is to inform the customer and present alternatives. A soft decline is ambiguous: the payment cannot proceed under the current conditions, but the conditions may change. The correct response depends on which soft decline reason code was returned and what the agent knows about the customer's situation. An agent without explicit decline code parsing cannot distinguish these cases. It treats the soft decline as a hard decline, stops the payment flow, and informs the customer that the payment failed - when in many cases a simple retry or a brief interval would have resulted in a successful transaction.

The lost revenue from mishandled soft declines in e-commerce is estimated to represent 1-3% of total revenue for affected merchants. This is not a small edge case. It is a systematic failure mode with direct revenue impact, and it is caused by a verification gap: the agent verified that the payment did not succeed on the first attempt, but did not verify the reason for that non-success or the appropriate response to it.

Implementing soft decline handling in payment agents

Soft decline handling requires adding three capabilities to the payment agent's toolset. First, a decline code parser that maps card network response codes to action categories (immediate retry, interval retry, customer action required, SCA required, permanent decline). Second, a retry orchestrator that implements the appropriate strategy for each action category, with exponential backoff and attempt counting to prevent retry spirals. Third, a verification step after each retry attempt that reads the actual outcome rather than assuming success on a 200 response. Together, these convert the binary success/fail verification model into a decline-type-specific verification model that handles the full range of payment outcomes correctly.

Decline code categories and required agent responses

| Decline category | Example codes | Common cause | Required agent response |

|---|---|---|---|

| Retryable (immediate) | 05, 51, 61 | Network timeout, temporary limit | Retry up to 3x with exponential backoff |

| Retryable (interval) | 01, 65 | Insufficient funds, daily limit | Retry after 24-48 hours |

| Customer action required | 78, N7 | Card update needed, CVV mismatch | Request customer to update payment method |

| SCA required (EU) | 1A | 3DS authentication required | Initiate 3DS challenge flow |

| Hard decline | 04, 14, 41, 43 | Fraud, closed account, stolen | Do not retry, present alternatives |

Soft declines sit quiet until a payment agent retries the wrong one; a frontier model inherits the missing category, at real cost. (arXiv:2602.06718)

VibeModel's Pattern Intelligence Layer identifies which decline code categories your payment agent is currently mishandling based on the pattern of transactions where a retry would have succeeded but was not attempted. By correlating decline code distribution with subsequent transaction outcomes for the same customers on the same cards, it quantifies the revenue impact of each mishandled soft decline category. That converts the soft decline handling investment from a nice-to-have to a specific business case with a dollar figure attached.

Frequently asked questions

How do we get access to specific decline codes from our payment processor?

Most payment processors expose decline codes in the payment response object but do not surface them in default error handling - they may be in a raw response field, an acquirer response code, or a network-specific message field. Review your processor's API documentation for the specific response object structure and test with your processor's sandbox environment to confirm which codes are returned for each scenario.

Should we tell the customer about the soft decline or just retry silently?

It depends on the retry timeline. Immediate retries (within seconds) can be transparent. Interval retries (24-48 hours) should include customer notification of what is happening and an option to update their payment method. SCA retries require customer involvement by definition. Customer transparency on payment status reduces support contacts and maintains trust even when the first attempt did not succeed.

Does this apply to recurring billing agents as well as one-time payment agents?

Yes, and it is particularly important for recurring billing where soft declines on subscription renewals require specific dunning strategies. Subscription billing platforms like Stripe Billing and Chargebee have built-in soft decline retry logic that follows card network guidelines - using these rather than implementing custom retry logic reduces the engineering burden while ensuring network-compliant behavior.