Even a frontier-model finance agent reads a "confirmed" API response as money moved, when it usually means only authorized. The IMF's 2026 review of agentic payments warns that autonomous agents act on the acknowledgment while settlement, reconciliation, and compliance resolve later in separate systems, so a confident "done" can sit on funds that never actually moved (IMF, How Agentic AI Will Reshape Payments, 2026).

Key facts.

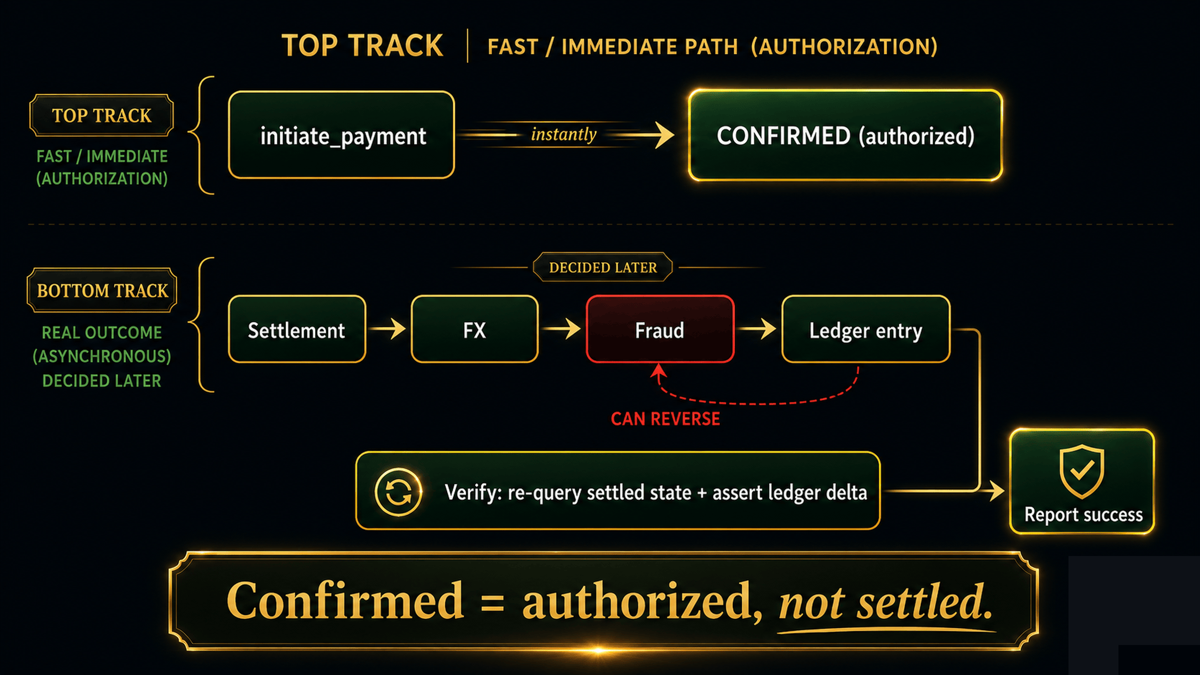

- A payment confirmation is the first step of a chain, not its end: authorization, settlement, FX, fraud review, and the ledger entry resolve afterward in separate systems on their own timelines, any of which can reject or reverse it (IMF, 2026).

- Financial actions are multi-system and eventually consistent: a near-duplicate invoice, a partial payment, a missing remittance reference, or an intercompany leg can all clear as success while the books do not balance.

- Re-querying settlement and reconciling safely needs an idempotency key, so a verification or retry references the same logical transaction and cannot itself trigger a second payment (IETF Idempotency-Key header).

Why is a confirmation not the outcome in finance?

Confirmed is authorized, not settled; a more capable agent exits on the same ack, then restates it later. (elibrary.imf.org)

Because the confirmation is the first step of a chain that finishes elsewhere. A payment API that returns confirmed has usually accepted or authorized the request, not settled it. Settlement, currency conversion, fraud review, and the ledger entry happen afterward in separate systems, on their own timelines, and any of them can delay or reverse the transaction. The business outcome that matters, money actually moved and the books reconcile, is a downstream state the agent never queries. So when the agent treats confirmed as done, it is reporting an acknowledgment as a settled fact: the immediate response looks like success while the end state is still undecided in another system.

What does the reconciliation gap actually cause?

Quiet financial errors that surface as restatements. A transfer reported successful that later fails settlement leaves a record saying paid against funds that never moved. A confident match on a near-duplicate invoice, same vendor, nearly the same amount, clears a queue and pays twice. A compliance check that resolves after the agent exits leaves a flagged transaction marked clear. None of these throw an error at the moment the agent acts, because the agent only saw the confirmation, so they emerge later in reconciliation, in an audit, or in a customer dispute. In regulated finance, a confident success without verification is not a small bug; it is a potential restatement or compliance event waiting to be found.

# In finance, verify the settled state. Re-query, reconcile, idempotently. ack = initiate_payment(amount, payee, idempotency_key=key) # returns "confirmed" = authorized settled = await get_payment_status(ack.id) # separate system, decided later assert settled.state == "SETTLED" assert ledger_delta(account) == amount # the books actually balance # Only now report success. Idempotency key makes the re-query/retry safe.

How do you close the reconciliation gap?

Make verification a mandatory step after every financial action, not an optional one. Re-query the downstream system for the settled state by transaction ID, run the reconciliation that asserts the expected ledger delta actually occurred, and only then report success. Encode business invariants as oracles, the funds moved, the books balance, the compliance flag cleared, and check them explicitly. Use idempotency keys so the verification re-query, or any retry, cannot trigger a second payment (IETF Idempotency-Key header). Require human approval above a materiality threshold, and trace the full path so a settlement that silently fails is caught in minutes. The agent then confirms that money moved, instead of confirming that an API agreed to try.

What the agent saw versus what it must verify

| Agent saw | What it meant | Verify instead |

|---|---|---|

| Payment confirmed | Authorized, not settled | Settled state via re-query |

| Transfer initiated | Accepted for processing | Funds moved, ledger reconciled |

| Invoice matched | Near-duplicate cleared | Unique match, no double payment |

| Compliance returned | Check started | Flag actually cleared |

| No exception | API accepted it | Books balance, invariant holds |

The pattern is that in finance the tool's confirmation is an acknowledgment, not a settled outcome, and the work that matters, settlement, reconciliation, compliance, finishes in systems the agent never queries. Verify the settled state and the ledger invariant before reporting success, idempotently so verification cannot double-pay, and a confirmation stops being a future restatement. Asserting the business outcome rather than trusting the acknowledgment is reliability at the pattern level, which is what VibeModel builds as the Pattern Intelligence Layer.

Frequently asked questions

Why isn't a payment API's confirmed status enough?

Because it usually means authorized or accepted, not settled. Settlement, FX, fraud, and the ledger resolve afterward and can reverse it, so verify the settled state downstream before declaring success.

How do I verify without risking a double payment?

Use idempotency keys so a re-query or retry references the same logical transaction and cannot trigger a second one. Then assert the settled state and the expected ledger delta.

What is the single must-have control in finance agents?

A mandatory post-action reconciliation that asserts the funds moved and the books balance, plus human approval above a materiality threshold. Confidence in the tool response is not verification.