Key facts.

- A 2025 position paper argues finance-agent evaluation overlooks risk and auditability, which determine deployability in regulated settings, in favor of accuracy and returns. source

- Regulated financial services require institutions to explain and defend the basis of decisions, especially in lending and trading. source

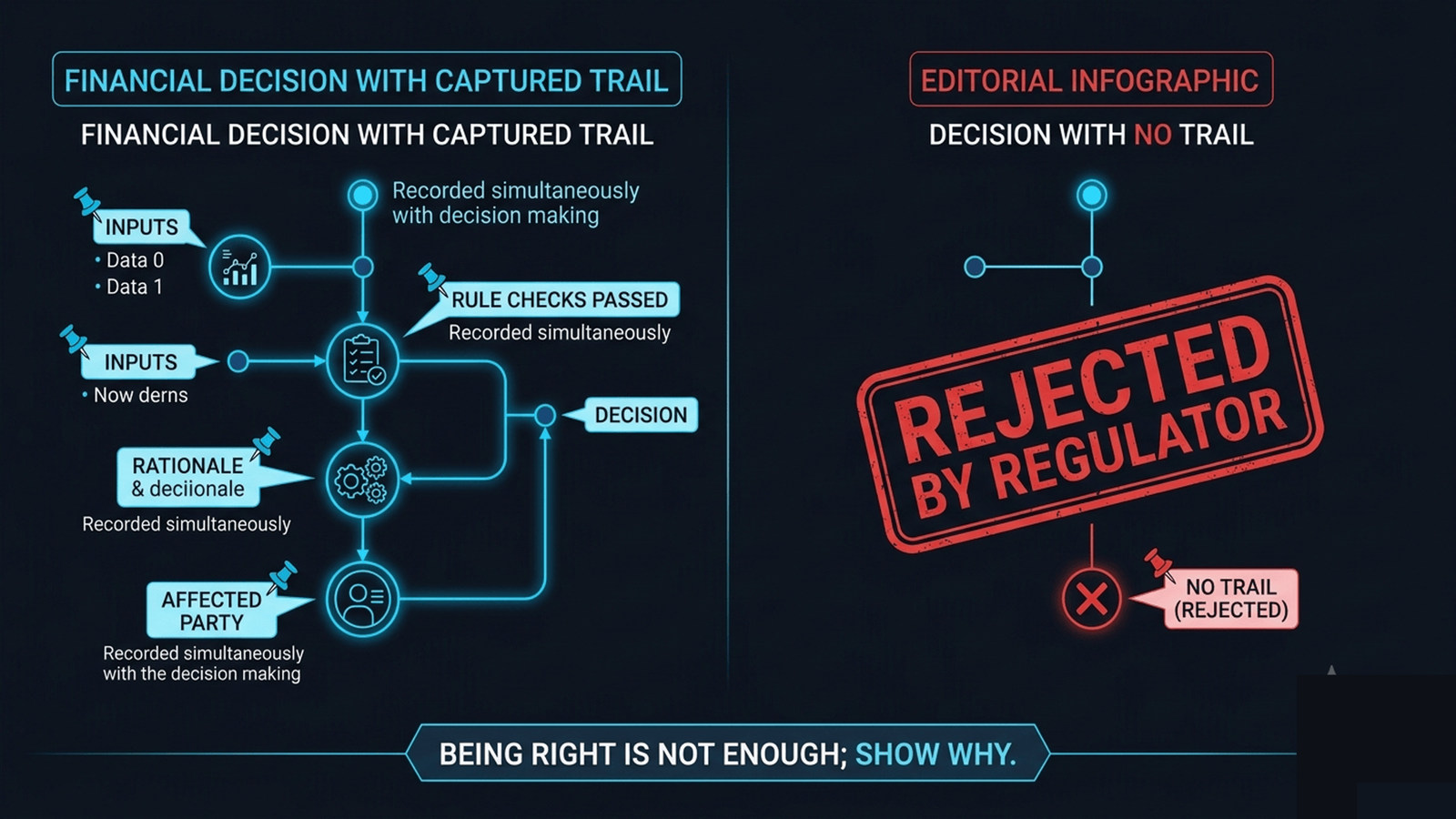

- An agent's after-the-fact explanation is a reconstruction, not a record, so the audit trail must be captured as the decision happens. source

Why isn't accuracy enough in regulated finance?

Finance benchmarks chase accuracy over auditability; a more capable agent that cannot explain why is undeployable, the cost paid late. (arXiv:2502.15865)

Because regulation asks a different question than accuracy answers. Accuracy tells you the agent was right; regulation asks you to demonstrate why it decided what it did, who it affected and that the decision met the rules and an accurate agent that cannot produce that demonstration fails the regulatory test regardless of its correctness. A lending decision must be explainable to show it was not discriminatory; a trading decision must be reconstructable to show it complied with the rules; any consequential financial action must carry a defensible rationale. The position paper's argument that finance-agent evaluation overlooks auditability is precisely this gap: teams optimize the accuracy number and discover at deployment that the regulator does not care how accurate the agent is if they cannot see why it acted. The explanation is the deployment requirement and an agent built only for accuracy did not capture it.

The record has to be captured as the decision is made, not reconstructed later, because an agent asked after the fact why it decided something produces a plausible new explanation rather than a faithful account of its actual reasoning. In a regulated audit, a reconstructed rationale is not the same as a recorded one and only the recorded one defends you.

What does a regulated audit trail capture?

The inputs to the decision, the rules and checks it passed, the rationale behind it and who or what it affected, recorded as the decision happens and stored so it can be produced on demand. Enough that an auditor can reconstruct not just what the agent did but why it was justified under the rules. This is a different artifact than accuracy and it has to be designed in, because the position paper's point is that teams measuring accuracy alone arrive at deployment without it. In regulated finance, the agent that can explain and defend every decision is deployable and the one that cannot, however accurate, is not.

| What the agent provides | Regulated deployability |

|---|---|

| Accuracy, no audit trail | Undeployable, cannot show why |

| Recorded rationale and rule checks | Deployable, decisions defensible |

Capturing that defensible record is part of what VibeModel does as the Pattern Intelligence Layer. We model the patterns of an auditable financial decision, the inputs, the rule checks, the rationale, recorded as it happens, so a regulated financial agent can explain and defend every decision rather than just be accurate.

Frequently asked questions

Why does the regulator care about why, not just what?

Because regulated decisions must be shown to be fair and compliant. A correct decision you cannot justify still fails the audit.

Can the agent explain after the fact?

Only as a reconstruction, which is a fresh plausible account, not a faithful record. The audit trail must be captured as the decision is made.

What must the trail contain?

The inputs, the rule checks passed, the rationale and who it affected, recorded live and producible on demand.